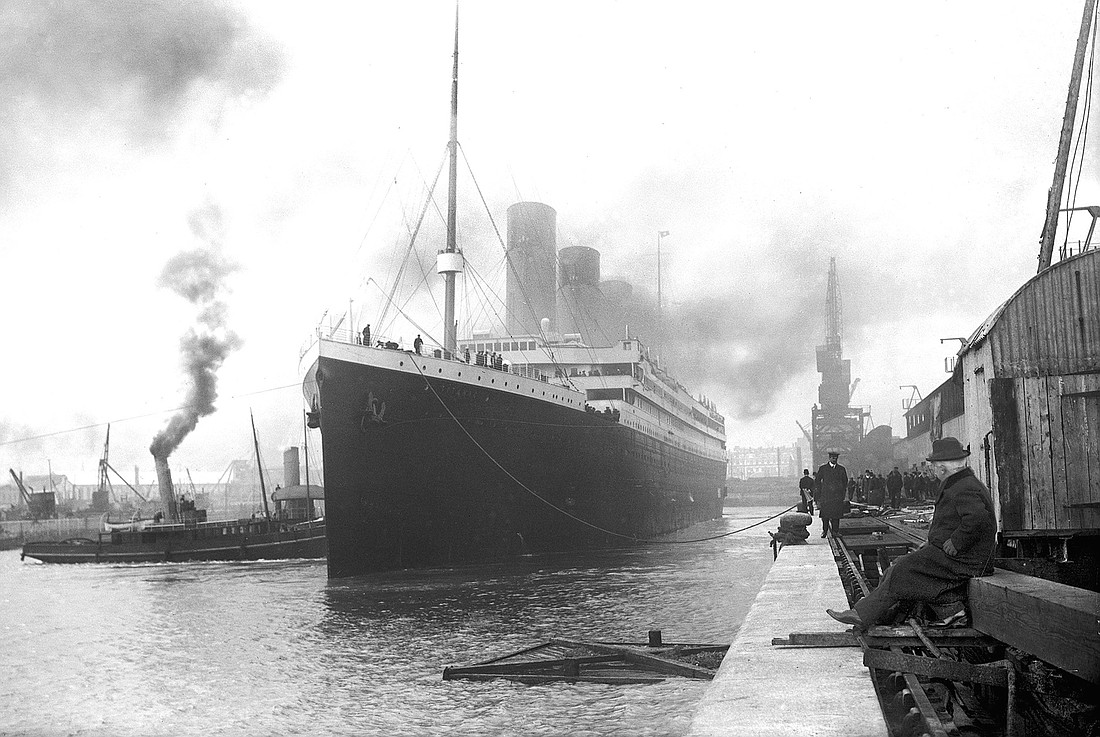

The two-year bankruptcy saga in a Jacksonville courtroom over artifacts from the RMS Titanic appears close to a resolution.

U.S. Bankruptcy Judge Paul Glenn approved an order last week setting an auction in October for the artifacts owned by Premier Exhibitions Inc. The assets will be sold together to the highest bidder.

Premier, which owns 5,500 artifacts from the famed ocean liner that sank in 1912, filed for Chapter 11 bankruptcy reorganization in June 2016.

Premier valued the collection at $218 million when it filed its bankruptcy petitions, but a consortium of hedge funds has submitted an offer of $19.5 million to buy the assets, which will be treated as the bid floor.

The auction is scheduled for Oct. 11 and a hearing is scheduled in U.S. Bankruptcy Court in Jacksonville for Oct. 18 to approve the winning bid.

Premier, which listed $12 million in unsecured debt in its court filings, had hoped to pay off its debts by selling a limited portion of its collection.

However, Glenn rejected that plan two years ago because of a 2011 federal court decision in Virginia that restricted the sale of Titanic artifacts in the interest of preserving history.

Glenn’s order last week said he would approve a sale that also is likely to be approved by the U.S. District Court in Virginia, which has an interest “in maintaining the integrity of the Titanic collection.”

The reorganization plan now estimates that unsecured creditors will receive 59 percent to 71 percent of their claims after the auction.

Stockholders of publicly traded Premier are unlikely to get anything.

Premier’s stock has continued to trade in the OTC market and was trading near the $5 level early this year before a previously scheduled auction to sell the assets was canceled.

The stock dropped sharply after that auction was canceled and was trading at 75 cents before Glenn’s order last week, which sent the stock below 50 cents.

Premier is headquartered in Atlanta but it filed for its Chapter 11 reorganization in Jacksonville because the company and some of its subsidiaries are incorporated in Florida.

Besides owning the artifacts, Premier’s business was producing museum-quality exhibits on the Titanic and other subjects.

An exhibit on the television show “Saturday Night Live” that turned out to be “incredibly unprofitable,” according to court documents, caused financial problems that led to Premier’s bankruptcy.

TapImmune Inc. filed an updated proxy statement last week setting its annual shareholders meeting for Oct. 16, when stockholders will vote on matters related to its proposed merger with Marker Therapeutics Inc.

Jacksonville-based TapImmune agreed in May to the merger of equals with Marker. Both companies are developing cancer therapy treatments but neither has products on the market.

According to financial projections in the proxy, TapImmune does not anticipate revenue until 2024 and Marker doesn’t expect it until 2025.

The merged company will be headquartered in Houston, where Marker has a relationship with the Baylor College of Medicine.

TapImmune moved its headquarters from Seattle to Jacksonville in 2015 when it began trials of a breast cancer treatment at the Mayo Clinic.

TapImmune has maintained a small headquarters office since moving and only had seven employees, according to its 2017 annual report.

The companies did not have a name for the merged company when the agreement was announced in May, but the proxy statement said it will be named Marker Therapeutics.

The original merger agreement called for shareholders of the two companies to end up with an equal number of shares in the company. But after a private placement of stock by TapImmune in June, a group of institutional investors will end up with 45 percent of the stock. Current TapImmune shareholders will end up with 27.5 percent, and Marker stockholders also will get 27.5 percent.

The merged company will be run by TapImmune’s executive team, including CEO Peter Hoang. The board of directors will comprise three members each appointed by the two companies.

Even without any sales in the foreseeable future, investors are encouraged about the potential of the merged company. TapImmune’s stock has risen from about $3 when the merger was announced to between $9 and $10 recently. The stock has traded as high as $13.55 since the merger agreement was signed.

TapImmune trades under the ticker “TPIV” but after the merger, it expects to trade under the symbol “MRKR” on the Nasdaq Capital Market.

The merger is expected to close in the fourth quarter this year.

SharedLabs Inc. last week filed an updated prospectus with the Securities and Exchange Commission saying it intends to sell 2.5 million shares of stock at $5 to $7 each in its initial public offering.

The Jacksonville-based IT services company first filed for an IPO in May but did not detail how much stock it wanted to sell.

Since its first filing, SharedLabs received Jacksonville City Council approval for more than $100,000 in incentives to move its headquarters to the Dyal-Upchurch Building Downtown at 6 E. Bay St. and create 107 jobs.

The updated prospectus lists the company’s headquarters address at that building, after it was previously headquartered in the Schultz Building at 118 W. Adams St.

SharedLabs said in its incentives application that it only had six local jobs, but its prospectus said the company had 567 employees as of Aug. 31 with additional offices in five states and Montreal.

The incentives agreement calls for the company to create the first 31 local jobs by the end of 2019.

SharedLabs reported revenue of $36 million and a net loss of $3.1 million in the first six months of this year, according to the prospectus.

The company expects about $13.6 million in net proceeds from the IPO if it sells the shares at the midpoint of its target range. It plans to use the proceeds for general purposes including expansion of the company and a possible acquisition.

The company was formed in 2016 and had no revenue until completing two acquisitions in 2017.

Besides the new shares issued in the IPO, current stockholders have filed plans to sell up to 1.1 million of their shares.

Investment firm Race Holdings LLC is SharedLab’s second largest stockholder with 2.125 million shares, or 24.5 percent of the stock. The original IPO filing said Race was looking to sell all of its shares but last week’s filing said it now plans to sell only a portion and retain 16.7 percent of the company after the IPO.

CEO Jason Cory is the largest stockholder with 2.55 million shares, or 31.9 percent of the stock. He has not filed plans to sell any of his holdings.

SharedLabs plans to list its stock on the Nasdaq Capital Market under the ticker “SHLB.”

No date has been set to bring the IPO to the market.

International Baler Corp. reported sales dropped 35 percent in the third quarter ended July 31 to $2.02 million.

The Jacksonville-based company, which makes balers used for recycling and waste disposal, reported net income of $4,939 in the quarter, down from $81,134 the previous year.

International Baler said in its quarterly report filed with the SEC that shipments of balers and conveyors fell in the quarter because of market conditions, including lower prices for recycled materials.