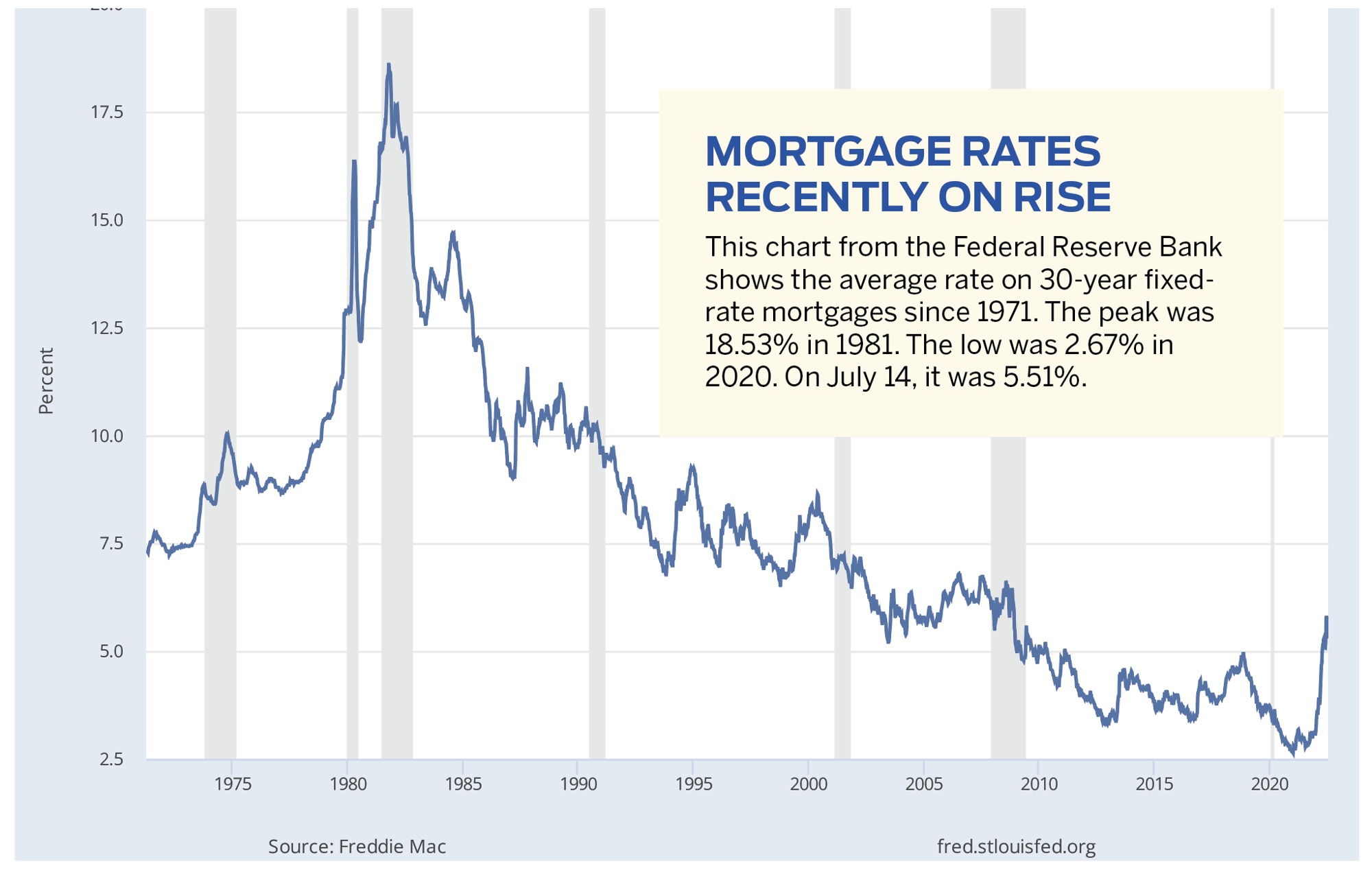

After saying in June it was cutting jobs in its mortgage lending business, JPMorgan Chase & Co. reported midyear results that show a big drop in mortgage activity.

The global banking giant said July 14 that its volume of mortgage loans originated in the first half of this year fell 41% to $46.6 billion, and its net revenue from home lending fell 26% to $1 billion.

The New York-based bank has a large mortgage operations center at 7301 Baymeadows Way in Jacksonville it acquired from the failed Washington Mutual Inc. in 2008.

JPMorgan Chase confirmed reports last month that it was cutting jobs because of “cyclical changes in the mortgage market.” However, it would not give details on how many jobs in Jacksonville were impacted or how many employees it has in Northeast Florida.

JAXUSA Partnership, the economic development division of JAX Chamber, reports the company has 3,900 area workers.

JPMorgan Chase said it is trying to reassign affected mortgage workers into other positions in the company.

Besides its mortgage center, the company began opening bank branches in Northeast Florida under the Chase brand in 2013.

Chase has 20 branches in the Jacksonville metropolitan area, according to the Federal Deposit Insurance Corp.

Wells Fargo & Co., another major bank with a big Jacksonville presence, also reported a drop in mortgage lending volume.

The San Francisco-based bank said its mortgage originations fell 31% in the first six months of the year to $72 billion and its mortgage banking income fell 63% to $980 million.

“The mortgage market is expected to remain challenging in the near term, and it’s possible that we have a further decline in mortgage banking revenue in the third quarter,” Chief Financial Officer Mike Santomassimo said in Wells Fargo’s July 15 conference call with analysts.

“We are making adjustments to reduce expenses in response to the lower origination volumes, and we expect these adjustments will continue over the next couple of quarters.”

Wells Fargo has filed notices with officials in Iowa about layoffs in that state, where its mortgage division is headquartered, but has not filed any layoff notices in Florida.

The company has the largest bank branch network in the Jacksonville area with 42 offices, according to the FDIC.

JAXUSA Partnership lists Wells Fargo with 1,450 employees in Jacksonville.

Wells Fargo reported its total headcount fell by almost 6,000 in the first six months of the year to 243,674.

JPMorgan Chase’s total headcount rose in the first half of the year by more than 7,000 to 278,494.

The company did not address changes in its mortgage business in its conference call.

While higher interest rates are deflating the mortgage market, credit card business is up at major banks.

Credit cards are the main Jacksonville business for Citigroup Inc. The company has operated a credit card operations center in Jacksonville since 1997 when it bought AT&T’s Universal Card business.

JAXUSA Partnership reports Citigroup has 4,000 Jacksonville employees.

“The positive drivers we saw in our two credit cards businesses over the last few quarters converted into solid revenue growth this quarter, most notably a 10% growth in branded cards,” Citigroup CEO Jane Fraser said in the company’s July 15 earnings news release.

As revenue in Citi-branded cards grew to $2.2 billion, spending by customers on those cards rose 18% from the second quarter of 2021 to $121.8 billion.

JPMorgan CEO Jamie Dimon also cited strong credit-card growth in his company’s quarterly news release.

“Combined debit and credit card spend was up 15% with travel and dining spend remaining robust. Card loans were up 16% with continued strong new account originations,” he said.

Johnson & Johnson said July 19 second-quarter sales at its Jacksonville-based vision care products business rose 4.9% to $1.24 billion.

However, adjusted for foreign currency fluctuations, sales were up 10.9% in the quarter.

Sales of the company’s contact lenses made in Jacksonville rose 2.9% to $894 million but adjusted for currency, sales rose 9.2%.

The New Jersey-based company said total adjusted sales rose 8.1% to $24 billion. Adjusted earnings rose by 11 cents a share to $2.59.

Fidelity National Financial Inc. said in a July 12 Securities and Exchange Commission filing that Roger Jewkes transitioned from his role as chief operating officer to the role of executive vice president.

The filing gave no other details.

Jewkes, listed in Fidelity’s May proxy statement as 63 years old, has been with the company since 1987 and became COO in January 2016.

The proxy listed him as the third-ranking executive for the Jacksonville-based title insurance company, behind Executive Vice Chairman Raymond Quirk and CEO Michael Nolan.

The high inflation environment could benefit a company like Fidelity National Information Services Inc., or FIS, according to Wells Fargo analyst Jeff Cantwell.

However, Cantwell downgraded his rating on the Jacksonville-based financial technology company as he becomes more selective on stocks in the industry.

“As Fintech CEOs and CFOs discussed throughout 2Q, fundamentals generally remain solid across the space. Recall inflation often is a positive for Fintechs near-term, particularly for payments companies,” Cantwell said in an update on the industry ahead of second-quarter earnings reports.

He expects the companies to report strong second-quarter results “unless something dramatic happened in June — which we don’t see materializing.”

While higher prices would benefit FIS’ merchant payment processing division, Cantrell has concerns about the company’s bank technology business.

“We think revenue growth from that channel (core processing) will likely start to decelerate next year,” he said.

FIS outperformed the market since the end of the first quarter, falling about 4% while the S&P 500 index fell about 8%, Cantrell said.

But as he looks for more selective opportunities in the industry, Cantrell downgraded FIS from “overweight” to “equal weight.”

He lowered his price target on the stock from $132 to $101, with the stock trading at $93.58 at the time of his July 14 report.

Another Wells Fargo analyst, Seth Weber, initiated coverage of Jacksonville-based Dun & Bradstreet Holdings Inc. with an “overweight” rating.

“Two years into a new playbook, with the post-LBO heavy lifting and large acquisition in the rearview, we see DNB poised for improving results,” Weber said in his research report.

“Whereas DNB’s traditional commercial end markets might lack the sizzle of some info peers, we see it as relatively well insulated for a choppy macro environment and declining consumer sentiment.”

Dun & Bradstreet was acquired in a 2019 leveraged buyout by a consortium of firms led by Cannae Holdings Inc. and Black Knight Inc., two companies spun off from Fidelity National Financial.

The business data company went public again in 2020 and moved its headquarters to Jacksonville in 2021.

“The 2019 take-private (deal) was a catalyst for needed change, which we believe has the company in a significantly better place relative to the predecessor, where underinvestment and ineffective strategy contributed to inconsistent financial performance,” Weber said.

He said the company’s history suggests it will be able to weather a potential recession.

“Amid a choppy macro environment and rising interest rates, we like DNB’s corporate exposure relative to consumer, mortgage, etc.,” he said.

“During the Great Recession, DNB’s revenue declined about 2% in 2009, outperforming the S&P and the traditional credit bureaus. We expect similar resilience ahead.”

Weber set a $21 price target, with the stock trading at $14.42 at the time of his July 12 report.

American Outdoor Brands Inc. dropped to a record low July 15 after reporting a sharp drop in sales and earnings.

The outdoor products company said sales in the fourth quarter ended April 30 fell 28.8% to $45.9 million and adjusted earnings fell to 14 cents a share, from 34 cents the previous year.

The company spun off from gunmaker Smith & Wesson Brands Inc. fell as much as $1.39 to $8.03 on July 15. It had traded as high as $36.62 in July 2021.

Missouri-based American Outdoor Brands includes the business of a Jacksonville company called Ultimate Survival Technologies, which Smith & Wesson acquired in 2016.

The acquisition was part of a plan to diversify from the firearms business. However, Smith & Wesson decided to spin off the outdoor products business not long after it closed its Jacksonville facility in 2019. The spinoff was completed in 2020.

Atlanta-based Pye-Barker Fire & Safety said July 12 it acquired Orange Park-based Bender & Modlin Fire Sprinkler.

Bender & Modlin, founded in 1999, provides commercial and industrial fire sprinkler and protection systems.

Pye-Barker, which has 120 locations and 3,000 employees, said Bender & Modlin will retain its name, leadership and employees.

Terms of the deal were not announced.

Tulsa, Oklahoma-based BlackHawk Industrial said July 14 it acquired Jacksonville-based Cornerstone Supply.

BlackHawk, an industrial distributor focused on metalworking, said the addition of Cornerstone and two other acquisitions in Idaho and Montana help it expand its capabilities across the country.

Terms of the deal were not disclosed.