The recovery from the housing market collapse a decade ago was slow, particularly in Florida, which was labeled king of the foreclosure market in the aftermath.

Florida was leading the nation in foreclosures in the early 2010s and Jacksonville and several other major Florida cities consistently ranked in the top 10 in the nation for the number of foreclosed properties.

However, the long recovery has finally come to fruition, according to Jacksonville-based mortgage technology firm Black Knight Inc.

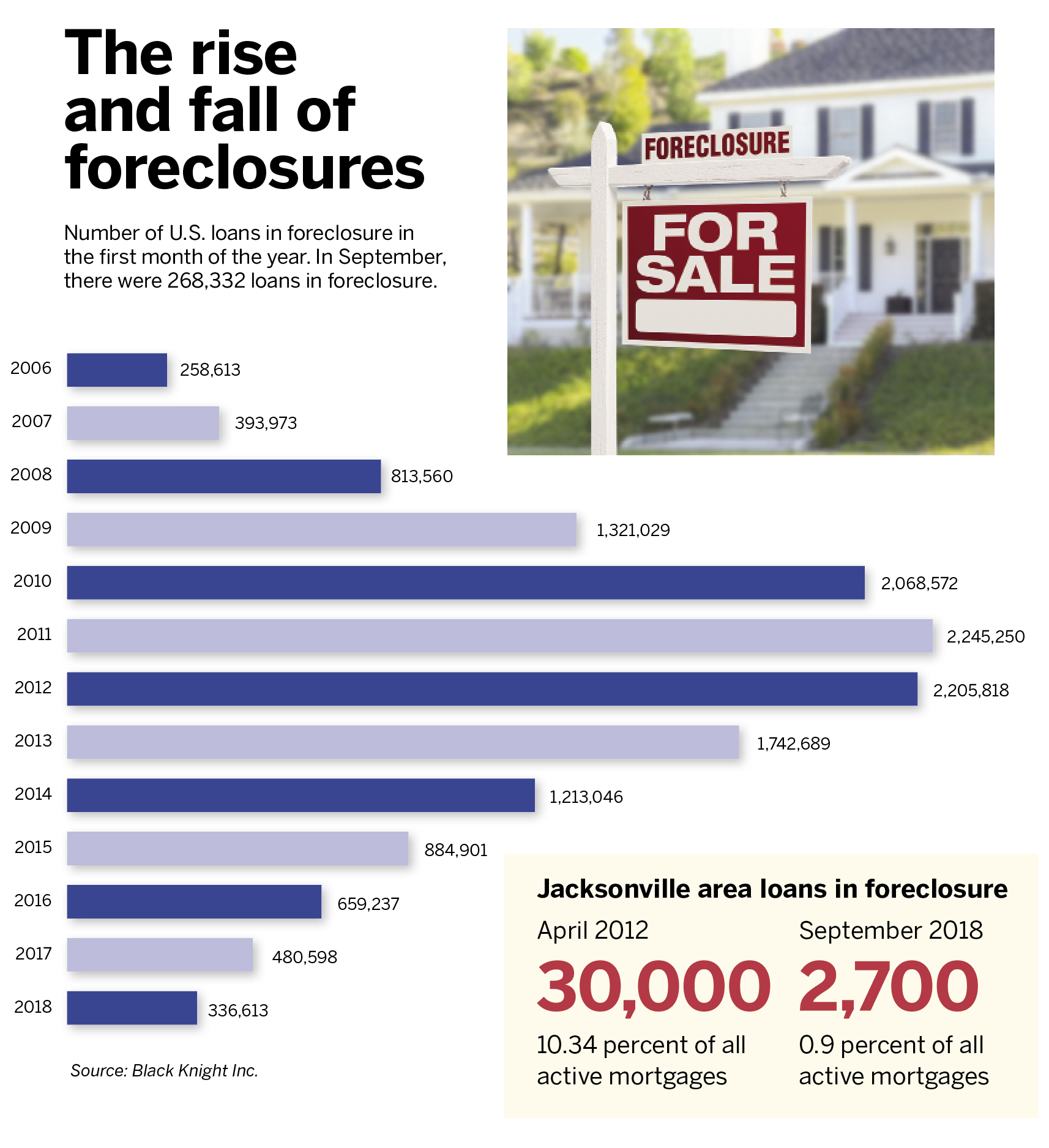

Black Knight’s Data & Analytics division last week reported the number of U.S. loans in foreclosure has fallen back to prerecession levels.

The number of loans in active foreclosure, which reached more than 2.2 million at its peak in 2011-12, fell to 268,332 in September, Black Knight said, the lowest level since 2006.

That puts only about 0.52 percent of all U.S. mortgage loans in foreclosure, down from more than 4 percent during the peak.

Jacksonville’s foreclosure market has improved tremendously since the local area’s peak in 2012.

Black Knight said the number of loans actively in foreclosure in the Jacksonville metropolitan area is about 2,700, or about 0.9 percent of all active mortgage loans.

At the peak in 2012, there were about 30,000 loans in foreclosure in the Jacksonville area, or 10.34 percent of all mortgage loans.

Black Knight also said the most recent data showed 360 foreclosure starts in the Jacksonville area in September, down from about 2,800 per month in 2011.

Not all the news is good for homeowners in Black Knight’s monthly report. While more homeowners are able to pay their mortgage loans on time, rising interest rates over the past two years are hurting their wallets.

“Due to rising rates, some 6.5 million homeowners that previously could have benefited from refinancing their mortgages have missed that opportunity,” said Ben Graboske, executive vice president of the Data & Analytics division in a news release.

“This year alone, 2.2 million borrowers had the opportunity to see a 0.75 percent reduction on their first mortgage rates but did not take advantage of the reduced rates before increases to the 30-year fixed rate removed their incentive,” he said.

“So far in 2018, the average 30-year fixed mortgage rate is up 0.85 percent – with 0.35 percent of that rise coming over the last two months after remaining flat for much of the summer. The result is that the refinanceable population has been cut by more than half – 56 percent – since the start of the year.”

Increased mortgage rates also are impacting home affordability, Graboske said.

“The monthly principal and interest payment needed to purchase the average-priced home has seen a $190 per month increase since the beginning of 2018, an 18 percent jump,” he said.

“It now takes 23.6 percent of the median income to make monthly payments on the average-priced home, making housing the least affordable it’s been in nearly a decade. While still better than the 1995-2003 average of 25.1 percent, we’re close to a tipping point.”