If the city wants to pursue selling JEA, it now has an estimate of how much the city-owned utility is worth.

The city could net $2.9 billion to $6.4 billion after retiring debt obligations and addressing other issues, City Council and JEA board members were told Wednesday during a three-hour special joint meeting at City Hall.

Michael Mace, the managing director of Public Financial Management Inc., presented the numbers. JEA hired the firm for the analysis.

Mace said the gross sales price would be $7.5 billion to $11 billion, depending on how the market values the utility.

JEA provides electric, water and sewer services to nearly 1 million customers across Northeast Florida.

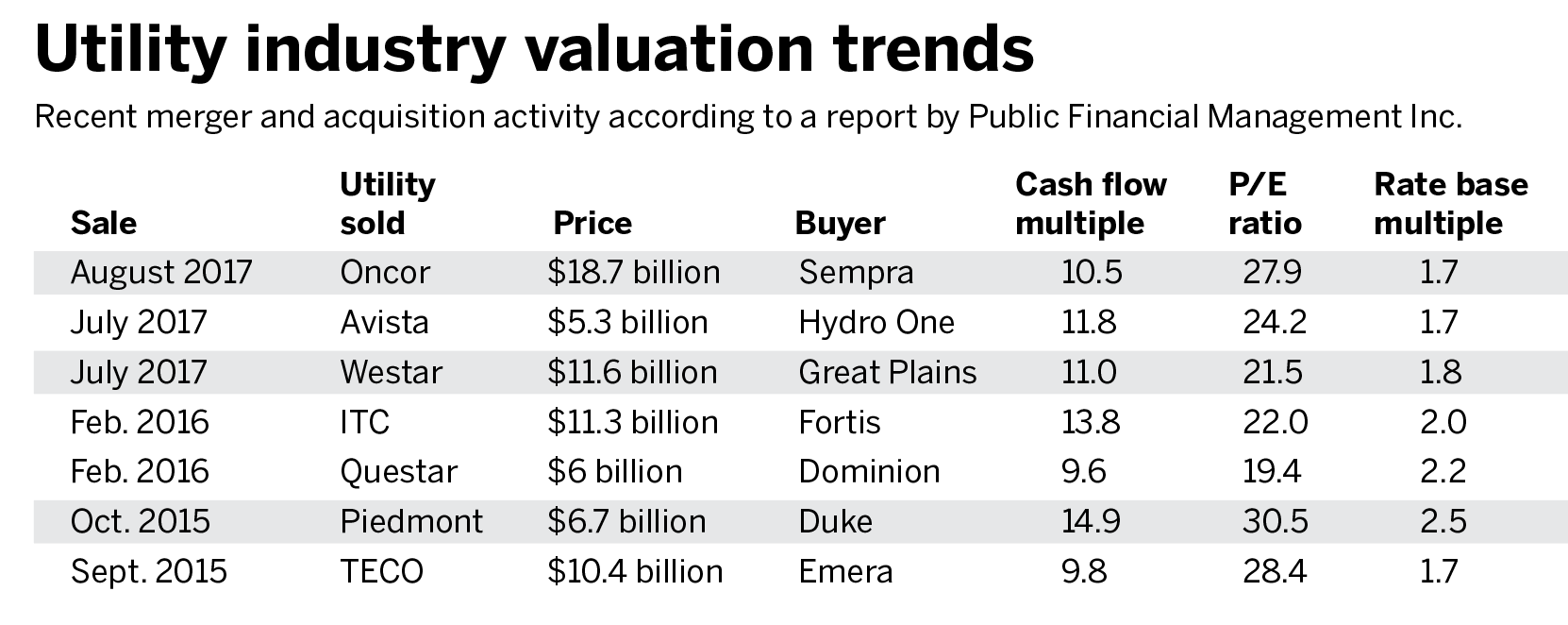

The financial audit outlines the methodology behind the evaluation and how JEA compares with other large utility sales in recent years.

Mace said the report was an “opportunity to provide new answers to old questions.”

The most recent look at JEA’s worth was in 2012, which found that a sale would result in the loss of 750 jobs with annual salaries and benefits totaling more than $70 million.

The new look at privatizing JEA came at the suggestion of former JEA board Chair Tom Petway during his final remarks to the board Nov. 28.

In a prepared statement, Petway “challenged” the board to consider privatization so it could better understand how such a change would impact employees, customers and the city’s coffers.

When asked to comment Wednesday, Petway declined and instead provided a copy of his Nov. 28 statement.

JEA board Chair Alan Howard said there was no recent discussion of selling JEA before the November meeting.

“To my knowledge, there has never been any board discussion of selling JEA prior to that, since the appointment of this board,” he said.

Howard said he did not expect the board to approve exploring a sale at its meeting scheduled for Tuesday.

The report

The report said factors boosting JEA’s value include its customer service marks from J.D. Power, a customer satisfaction analytics company; a strong, diverse and growing Northeast Florida service territory; and utility rates below the national average.

“In addition, there have been changes in JEA’s business outlook and financial structure that have JEA more appealing to potential purchasers of utility assets,” the report states.

JEA has about 464,000 electric customers spanning a 900-square-mile, three-county, six-municipality territory.

The company serves 346,000 water and 269,000 wastewater customers within four counties and serves an additional 11,000 customers with reclaimed water.

In addition, JEA’s District Energy System provides chilled water services to customers for air conditioning. The city is the largest user for some of its sports and entertainment facilities.

JEA’s electric operations are in the minority among its peers. Just 15 percent of the country’s more than 2,000 electric utilities are publicly owned. Water and sewage services are more common, with 80 percent owned by municipalities.

According to Mace, most U.S. customers purchase energy from for-profit, investor-owned utilities, which have an obligation to their shareholders to create profits and targeted equity returns.

The most notable difference between the two corporate structures is that investor-owned utilities pay state, federal, local and school taxes, while JEA pays a fee to the city’s annual budget in lieu of local taxes. For the 2017-18 budget year, that fee is roughly $116 million.

A private company still would pay the franchise fees and public service taxes that JEA now pays.

Valuing JEA

Mace’s report says the city could gross $7.5 billion to $11 billion on the sale of JEA, depending on market conditions.

“It would be optimistic to assume that the high-end of the price range is the most appropriate starting point for JEA price discussions,” the report states.

If JEA is sold, it would have to apply the proceeds to the utility’s $3.9 billion in outstanding debt.

JEA also would need to terminate about $100 million in interest rate swap contracts it has in place to hedge its variable-rate debt.

To efficiently transition to a new company, the report says JEA would use about $600 million to settle those obligations.

With those debts addressed, the city could net between $4.1 billion to $7.6 billion, the report says.

It says there’s also a chance the city would choose to address another obligation – a 20-year power purchase contract to source nuclear energy from the Alvin W. Vogtle Electric Generating Plant, also known as Plant Vogtle.

The plant is being built near Waynesboro, Georgia, and could be online by the mid-2020s.

According to Mace, if JEA is sold, the city may need to pay off some of that debt to comply with requirements related to its tax-exempt bonds and Build America Bonds issued for the project.

The obligation is roughly $1.2 billion.

That would bring the net proceeds to $2.9 billion to $6.4 billion, although those values could vary significantly depending on market conditions “and several variables that cannot be determined at this time.”

The report states that while it’s not uncommon to see transactions and the consolidation of large electric providers in the U.S., there have been a limited number of water and wastewater utility sales in recent years – at least compared to JEA’s footprint.

Mace said he believes that based on the values of those transactions, the open market could value JEA’s water and sewer infrastructure higher than some of its electric assets.

He said his company uses a price-to-earnings ratio to value what he calls a “Mid-Cap Integrated Utility,” like JEA, which has a potential market value between $2 billion and $10 billion.

The ratio measures the price owners and investors are willing to pay relative to the annual earnings they expect to receive on that investment.

Mace points out investors are paying more for utilities than ever before.

The reasons vary by case, but Mace said that access to relatively low interest rates on debt, lower capital costs and a steady rise in stock market value seem to be factors in each sale.

He also explains that asset prices for utility sales generally are expressed in terms of their values as multiples of earnings before interest, taxes, depreciation and amortization, or EBITDA, which represents cash flow, as well as “Net Property, Plant and Equipment,” which represents a utility’s rate base.

Since September 2015, the report indicates, those acquisition multiples have reached near record highs.

That, along with gains in the stock market, and the perception that JEA has plenty of opportunity for growth in Northeast Florida, “makes JEA an extremely interesting target for any utility seeking to provide value to its owner,” and that a nonutility investor could make a significant return on its investment.

Other challenges

JEA employs about 2,000 people in Jacksonville, with a majority working out of the Downtown headquarters at 21 W. Church St.

Last year, JEA signed new contracts with the five labor unions representing its employees, in conjunction with major pension reform legislation led by the mayor.

All those agreements include pay raises of at least 2 to 5 percent as compensation for the additional 8 to 10 percent employees contribute to a new retirement plan.

Any sale of JEA likely would have provisions guaranteeing employment for workers, or a commitment to maintain a physical office presence Downtown, at least in the short-term, to ensure a smooth transition and to maintain service quality for customers, according to the report.

One criticism of the audit is it doesn’t factor how JEA would pay $554 million in unfunded pension liability it still owes for employee pensions.

Howard seemed confident that a half-cent sales tax measure passed by council last year would address that obligation. He also said it could be worked out during negotiations, if they take place.

The values presented didn’t take into consideration the five interlocal and franchise fee agreements JEA has with Baldwin, Atlantic Beach and Orange Park for electric services and with St. Johns and Nassau counties for water and sewage services.

St. Johns and Nassau counties both would have the first right of refusal versus any private company vying to purchase the infrastructure in those counties, which would change JEA’s value, according to a memo describing how the city could legally move forward with a sale. that memo was issued Tuesday by city General Counsel Jason Gabriel.

Questions remain

The joint meeting was called by Curry after council President Anna Brosche declined to hold one of her own at the request of JEA CEO Paul McElroy.

Several council members said Wednesday they were left with more questions than answers and vowed to hold more public meetings to address their concerns.

Council member Reggie Brown wants assurance that any new buyer would address communities in Jacksonville that still don’t have access to JEA’s sewage infrastructure.

“We need a viable plan, a commitment,” Brown said. “Because people are paying stormwater credits and not getting services.”

Council member Danny Becton told Howard he believed “the cart is coming before the horse,” saying he was unsatisfied with the lack of reasons given to explore a potential sale.

Becton, along with council members Al Ferraro and Tommy Hazouri, questioned how a valuation was commissioned when council, the policymaking body, did not ask for one.

In response, Howard said that no one asked for the review outside of the Nov. 28 board meeting, but that establishing a value for JEA was worth the estimated $100,000 cost to conduct the report.

“If we put the cart before the horse, then that’s on me,” Howard said. “I take full responsibility.”

Howard said he was not for or against privatization, even if market conditions were ripe for one.

“This is a very preliminary inquiry,” Howard said after the meeting. “No one’s made a decision to sell JEA and no one’s made a commitment to sell JEA.”

For JEA to move ahead with exploring a sale, 13 of the 19 council members would have to approve amending language in the city Charter.

From there, a likely yearslong process would commence and require the sale to receive approval from federal and state regulators, council and the mayor.