By Katie Garwood & Mike Mendenhall • Staff Writers

Jacksonville organizations say they were able to keep their staffs employed because of loans they received from the federal Paycheck Protection Program.

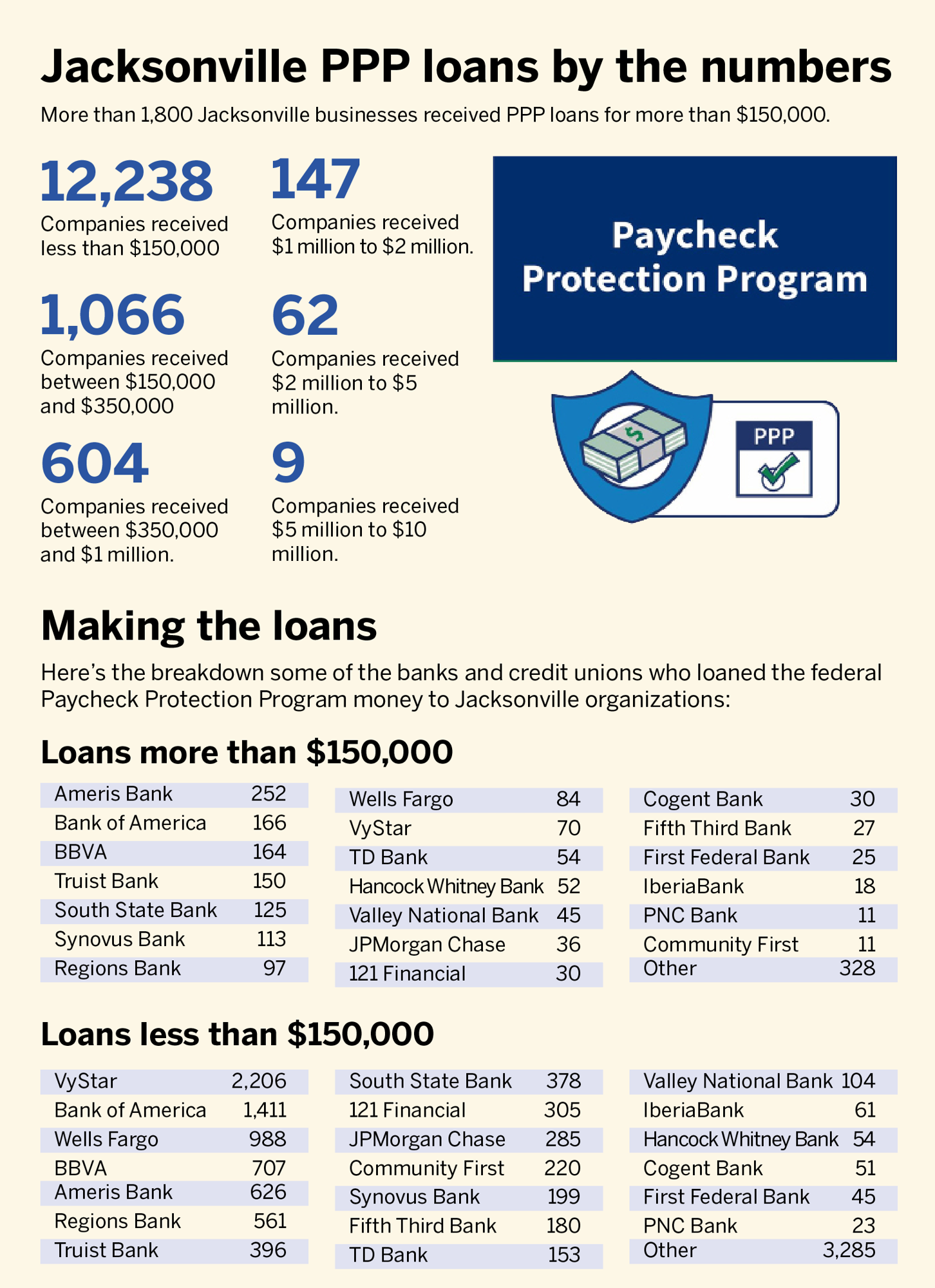

Nearly 135,000 Jacksonville jobs could be retained as a result of the Paycheck Protection Program, according to Small Business Administration data.

Only the identities of organizations that borrowed more than $150,000 were made public. The loans are forgivable if entities meet certain requirements.

If the requirements aren’t met, the remainder of the loan must be paid back with 1% interest over two or five years, depending on when the application was approved.

The PPP is an SBA loan designed to keep employees on the payroll. It can be forgiven if employees remain on the payroll and the money is used for eligible expenses, such as payroll, interest on mortgages, rent and utilities.

The amount an organization can receive is equal to 2.5 times its average monthly payroll, or $10 million, whichever is lower. Most received loans of less than $150,000 from the SBA.

Jacksonville entities receiving loans included businesses, nonprofits, schools and churches.

Nine organizations in Jacksonville received between $5 million and $10 million from the program. Stein Mart said in its first-quarter report it received a $10 million loan, the maximum. It did not list the number of employees on its payroll.

Alex Sifakis is co-owner of JWB Real Estate Capital LLC with company CEO Gregg Cohen, CFO Adam Rigel and COO Adam Eiseman.

Sifakis would not disclose the amount of the PPP loan the real estate investment company received, but the SBA data shows JWB Real Estate Capital received $150,000 to $350,0000.

Two other JWB affiliated companies also received PPP loans. JWB Property Management LLC was listed at $350,000 to $1 million and JWB Construction Group at $150,000 to $350,000, according to the SBA.

Sifakis said for JWB, the PPP accomplished its intent. JWB companies were able to keep all 80 employees on the payroll and hire six more people, he said.

JWB had no layoffs because of COVID-19 and Sifakis attributes much of that to PPP.

“With so much uncertainty, we didn’t know exactly what was going to happen,” he said. “Without it, less capital would have gone out into the community. It gave us the confidence to continue to invest.”

Michael Munz, a partner at The Dalton Agency, said in reviewing the guidelines for the program, the company felt it qualified and applied. It received between $1 million and $2 million.

The agency has offices in Jacksonville, Atlanta and Nashville.

Munz said the money was used in accordance with the program’s guidelines. The SBA requires the money to be used for payroll costs, mortgage, rent or utility payments.

He said the company was able to maintain the same number of employees.

“I don’t think we would have taken advantage of the opportunity to apply if we did not feel it was necessary, just like hopefully any company would,” Munz said.

Once organizations receive the loan, they also have the option to return the money.

CNBC reported July 6 that recipients canceled or returned about $30 billion in PPP funds nationwide.

The Bolles School, which according to SBA data received between $2 million and $5 million, returned the funds it received from the program.

Senior Director of Communications and Marketing Jan Olson said when the school applied for the program in early April it did not know what the financial impact of the pandemic would be like.

When the SBA released new guidelines for the program, the school felt it no longer qualified for the program and returned the funds, she said.

“Fortunately, the financial impact on the School was not as bad as our initial thoughts,” Olson said in an email.

The Jacksonville Daily Record’s parent company, Sarasota-based Observer Media Group, received $1.6 million from the program. Daily Record & Observer LLC in Jacksonville received $462,000 of the $1.6 million.