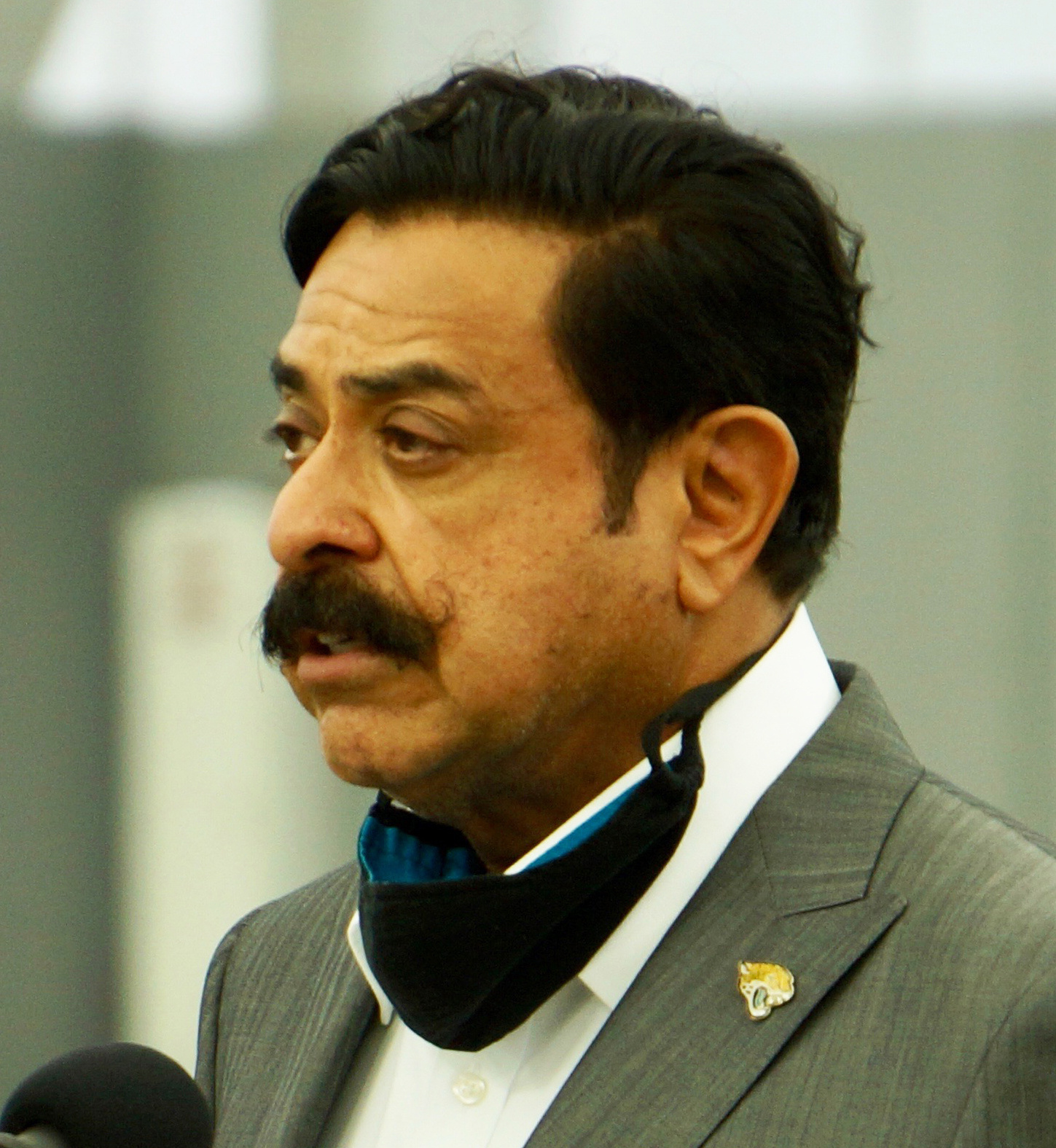

The Jacksonville Jaguars owner sees little success on the field, but is on the brink of a $450 million Lot J development.

Jacksonville Jaguars owner Shad Khan is ending the year with a losing 2020 season on the field but a $245.3 million taxpayer-backed investment for his proposed $450 million Lot J development on the table.

Khan’s milestone 100th loss Nov. 22 since buying the Jaguars in 2012 did not deter the 70-year-old Forbes 400 billionaire from pursuing his real estate ambitions in Downtown’s Sports and Entertainment District.

His entertainment, hotel, residential and retail Lot J project west of TIAA Bank Field with partner The Cordish Companies is up for City Council debate in early January.

Council President Tommy Hazouri said the deal will “probably pass” when it comes to a final vote, which is expected Jan. 12.

Lot J isn’t Khan’s only proposed project.

Jaguars President Mark Lamping told a Downtown Investment Authority Committee on Nov. 12 that Khan is “ready to go” on plans to develop Metropolitan Park and parts of the city-owned riverfront Shipyards, which includes a 171-room Four Seasons hotel with 20 for-sale condominiums.

Khan owns the Four Seasons Hotel Toronto and also would own the Jacksonville property.

DIA documents show Khan wants $151.2 million in city incentives for the Four Seasons/Metropolitan Park development comprising cash, loans, tax rebates, site infrastructure and land giveaways.

Another public incentive also surfaced: Khan will ask the city to partner on stadium improvements before the Jaguars’ lease ends in 2030.

Khan pledged to a nonprofit investment in the Shipyards when he announced a $5 million donation Nov. 16 to the Museum of Science & History’s capital campaign to relocate from the Southbank.

By Mike Mendenhall

Duval County Schools chief navigates a sales tax referendum, the pandemic and was named state Superintendent of the Year.

Duval County Schools Superintendent Diana Greene, on the job since July 1, 2018, led the system of more than 129,000 students during a pandemic, made budget adjustments and helped lead the successful campaign for a half-cent sales tax for improvements.

For those and more reasons, the Florida Association of District School Superintendents named Greene, 57, the 2021 Superintendent of the Year.

“Diana leads with compassion and conviction, driven by a work ethic grounded in servant leadership and a commitment to educational excellence. Her philosophy that the work of a superintendent and public educators ‘has to be done as if there is no tomorrow because we only get one chance with these kids’ clearly exemplifies her dedication to public education,” said Michael Grego, association president, in presenting the award.

Along with school board members, the local teachers union and much of the business community, Greene was among the leaders of the two-year campaign to establish a half-cent sales tax increase in Duval County that would provide about $2 billion over the next 15 years to improve the county’s public schools.

After City Council in August 2019 declined to approve placing the proposal on the ballot, the school board filed a lawsuit against the city for delaying the referendum.

Seven months later, the board dropped the lawsuit after Council took up the referendum again and approved putting it on the ballot.

The referendum was adopted by a 67% to 33% vote in the Nov. 3 general election. It will take effect Jan. 1.

The additional revenue is earmarked for safety and security, building upgrades and renovations at facilities throughout the county.

Greene also is credited with making improvements to budget forecasting and monitoring toward reducing or eliminating the level of reserves needed to balance the budget.

By Max Marbut

The president and CEO of Edward Waters College eliminated the institution’s operating cash deficit and grew enrollment.

The Edward Waters College board of trustees in August unanimously approved an extension of President and CEO A. Zachary Faison Jr.’s contract until July 2025. Faison, 40, signed his original five-year contract in 2018.

The action came eight months into a year of accomplishments for Jacksonville’s Historically Black College.

In 2020, Edward Waters College:

■ Eliminated its multimillion-dollar net operating cash deficit and achieved the institution’s first fiscal year-end operating net cash surplus in more than a decade.

■ Secured a $3.5 million increase in the recurring state funding allocation to $7.4 million, a 72% increase over previous years, paving the way for new academic courses including master of business administration, the college’s first post-graduate program.

■ Increased private gifts, pledges and in-kind support to $3.1 million, an increase of 30% in 18 months.

■ Formed a partnership with Follett Higher Education Group to furnish new laptop computers to every new first-time in college full-time student at EWC through the 2025 academic year.

■ Upgraded the learning management system including installation of new computer servers and more Wi-Fi access points.

■ Established the Center for Undergraduate Research and founded the Rev. Charles H. Pearce Summer Institute & Bridge Program.

■ Grew fall 2020 enrollment, despite COVID-19, to 969 students, a 4% increase from fall 2019 and the most students enrolled in more than 15 years. The college also retained 82.6% of eligible returning students.

■ With help from a $4.3 million grant from the city, began construction of a $4.3 million, 5,000-seat athletic stadium.

■ Was invited by the Southern Intercollegiate Athletic Conference to join the NCAA Division II conference and added the women’s soccer program and men’s and women’s indoor track programs.

By Max Marbut

The VyStar Credit Union CEO is boosting his company’s visibility and partnered with the city on a COVID-19 loan program.

VyStar Credit Union and its CEO, Brian Wolfburg, made a clear impact on Jacksonville this year, pressing on with developing its Downtown headquarters and helping small businesses in need amid the COVID-19 pandemic.

And in February, the credit union made a $2.5 million contribution to the Museum of Science & History’s campaign to build MOSH 2.0. Wolfburg then joined the museum’s board of trustees.

Wolfburg, 43, became CEO of the locally based credit union in 2017. In past years, he made similar commitments to developing Downtown Jacksonville and improving the community.

In 2018 and 2019, the credit union bought and renovated property at 76 S. Laura St. and 100 W. Bay St. for its headquarters and committed to moving 1,000 employees to Downtown Jacksonville. Wolfburg led an effort for VyStar to buy naming rights on what is now the VyStar Veterans Memorial Arena.

Despite challenging conditions in 2020, Wolfburg’s and VyStar’s commitment to the city didn’t waver.

When the pandemic struck in March and small businesses began to struggle, VyStar partnered with the city on an emergency loan program. VyStar made loans of up to $100,000 available to qualifying businesses with no payments due in the first year.

Meanwhile, Wolfburg’s efforts to redevelop VyStar’s headquarters continued. The West Bay Street building will house employees and, on the ground floor, The Bread & Board restaurant and a marketplace.

The credit union also started work on the breezeway between its parking garage and the office buildings.

Plans to build another VyStar parking garage, at Laura and Forsyth streets, are going through approvals.

VyStar proposes a nearly 300,000-square-foot, 798-space garage with ground-floor retail.

VyStar became a bright light in Downtown in a more literal sense this year, adding blue lighting to the top edges of the tower and adding a new dimension to the Jacksonville skyline.

By Katie Garwood

The Fidelity National Information Services Inc. chairman, CEO and president is expanding and building a new headquarters.

Gary Norcross spent 2020 leading a Jacksonville-based Fortune 500 financial services technology company that began building a $156 million Downtown headquarters tower and parking garage expected to be completed in June 2022.

The chairman, president and CEO needs the riverfront tower under construction at 347 Riverside Ave. in the Brooklyn neighborhood because of Fidelity National Information Services Inc.’s purchase of Cincinnati-based Worldpay Inc. in July 2019 for $48 billion.

FIS provides technology for financial institutions and Cincinnati-based Worldpay provides payment services.

“This transformative combination significantly enhances the scale, portfolio and global footprint of FIS to help our clients capitalize on growth opportunities at a time of rapid marketplace change,” Norcross said in a news release about the acquisition.

FIS now is based at 601 Riverside Ave., near the new headquarters site.

Florida Gov. Ron DeSantis joined Norcross on Nov. 1, 2019, to announce the headquarters project, one of the last major public economic development events before the 2020 pandemic shutdown started in March.

Norcross said FIS will create 500 jobs and retain the company’s 1,216-employee workforce.

The project led the Jacksonville Daily Record and the Jacksonville Record & Observer’s Top Construction Projects of 2020.

The Wall Street Journal said Dec. 20 FIS was contemplating an even bigger move to end 2020 by negotiating a potential $70 billion merger with Atlanta-based Global Payments Inc.

It would have been the largest deal of any business in 2020, but the Journal said negotiations broke down.

Norcross, 53, started his career with FIS when he joined Arkansas-based Systematics Inc., a predecessor company, in 1988 as an entry-level programmer.

After serving in other leadership roles, he was named FIS president and COO in 2012, president and CEO in 2015, and added the title of chairman in 2018.

With a bachelor’s degree in business administration from the University of Arkansas, Norcross leads the $12 billion global business.

Under his leadership, FIS has grown to more than 55,000 employees worldwide, serving more than 20,000 clients in more than 130 countries.

By Karen Brune Mathis

The CEO of Recency Centers Corp. started her job just two months before the COVID-19 pandemic struck.

On Jan. 1, Lisa Palmer became the only woman in Jacksonville to serve as a current CEO of a publicly traded company.

What a year it’s been.

Already strategizing the future of brick-and-mortar retail in the world of e-commerce, Palmer took over leadership at Jacksonville-based Regency Centers Corp. just two months before the pandemic shutdowns.

The spread of COVID-19 closed retailers and restaurants, which are the bread-and-butter of the company’s business. Regency Centers develops, owns and leases shopping centers.

Palmer, 52, came into the leadership role by working her way up the ranks. She joined Regency in 1996, became chief financial officer in January 2013 and president in January 2016. She remains president as well as CEO.

Knowing the business so closely helped the Wharton School MBA graduate steer it through the crisis.

As of May 5, Regency Centers collected 62% of April pro-rata base rent.

The company said that improved to 77% of second-quarter and 86% of third-quarter pro-rata base rent collected through Oct. 31.

In November, Regency Centers said trends are improving for its retail tenants as they recover from COVID-19 closings.

“As tenants are able to reopen, even with capacity restrictions, they gain the visibility they need to start paying their rent or to enter into a deferral plan that both they and we can feel confident in,” Palmer said.

Regency said businesses considered “essential,” including grocers, drugstores and medical services, produced the best results, with 98% of rents collected as of Oct. 31. The worst performance came from full-service restaurants.

As of Nov. 5, Regency’s 414 shopping centers had remained operating throughout the pandemic in compliance with government mandates. As of Oct. 31, about 97% of its tenants were open, while Regency executed rent deferral agreements on more than 1,300 leases. Repayments began in December.

Regency has been working to help its tenants adapt. Palmer said the company has confidence that many will emerge stronger.

By Karen Brune Mathis