Much of the public discourse associated with the Tax Cut and Jobs Act of 2017 is focused on the changes expected to reduce income taxes for individuals and corporations.

Those changes also are expected to reduce taxes paid by people who own businesses that aren’t structured as corporations.

Most businesses are defined under tax law as a “pass-through” entity, such as a partnership, limited liability company, S-corporation or a sole proprietorship. Under that structure, earnings from a business are “passed through” to the owner or owners, who pay taxes on the earnings as individuals.

In most cases, the new tax structure should reduce the taxes paid by owners.

Under the new law, owners of such businesses will be allowed when they file their taxes for 2018 to deduct 20 percent of their earnings, thereby reducing their taxable income compared to the structure in place for 2017 earnings, when taxes were due on 100 percent of earnings.

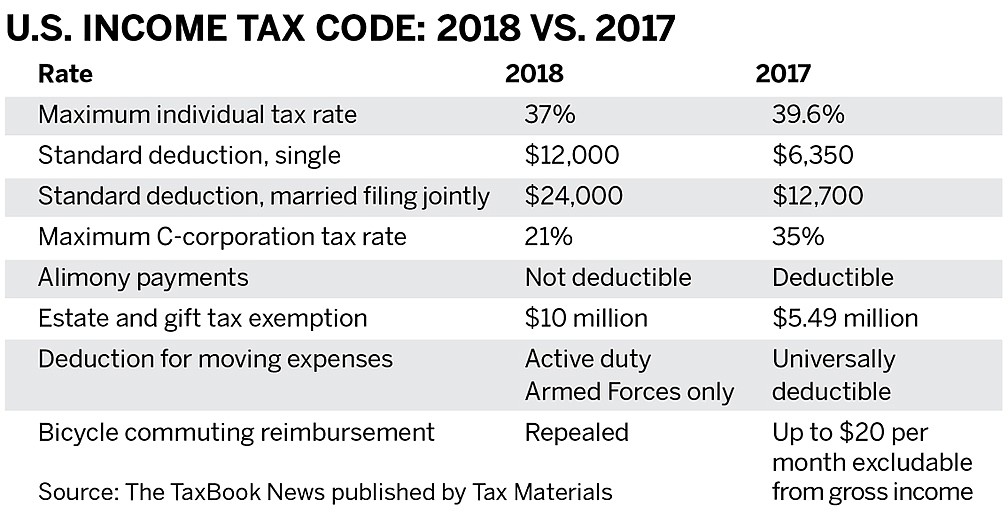

Reductions in the individual rate brackets based on income and the increased standard deduction under the new tax law will result in most people seeing an increase in take-home pay.

The key is the limit on pass-through income defined by the new law, said Jerry Jeakle, a CPA and partner at Hartman, Blitch & Gartside Certified Public Accountants.

Owners of pass-through businesses with taxable income less than $157,500 for a single filer or $315,000 if married and filing jointly, defined as “threshold amounts,” will qualify for the full 20 percent deduction.

However, if earnings are above the threshold, the maximum 20 percent deduction is reduced in steps to zero when earnings exceed $207,500 for a single filer and $415,000 for married filing jointly.

Jeakle said 95 percent of his clients are pass-through businesses, and most are small to medium in terms of earnings. The lower individual rates and increased standard deduction should result in a bottom-line reduction in taxes.

“It will be better for them if they get the 20 percent deduction,” he said. “The mom-and-pops will do the best under the new plan.”

Under the new law, businesses with earnings above the threshold amounts also do not qualify for the 20 percent deduction if the principal asset of the business is the reputation or skill of one or more of its employees or owners, or if it involves the performance of services including investment and investment management trading or dealing in securities, partnership interests or commodities.

That includes businesses in the fields of health, law, consulting, athletics, financial services and brokerage services – but architects and engineers will be allowed the deduction.

Stacy Byrd, a tax attorney at the Holland & Knight law firm who specializes in partnership tax matters, said the new tax law has some nuances when it comes to pass-through businesses.

For example, she said, for such businesses with earnings above the thresholds for single and married filing jointly taxpayers, the tax deduction may be capped at either the owner’s share of half of the entity’s total wages — or 25 percent of the entity’s wages plus 2.5 percent of the entity’s capital assets, whichever is greater.

That structure will benefit businesses with substantial payroll and businesses with few employees that have large sums of money invested in capital assets such as real estate, manufacturing and construction, Byrd said.

The new regulations as they apply to pass-through businesses with above average earnings may cause some business owners to consider dissolving their pass-through and reforming as a traditional C-corporation. Under the new law, taxes on 2018 earnings will be a 21 percent flat rate, compared to the previous tax of up to 35 percent.

“It will be worth looking at. It will be a closer call to decide if you’re a pass-through or a C-corporation,” said Peter Larsen, chair of the national tax practice group at the Akerman law firm.

He said the new law also changes the rules for international tax issues, estate taxes and other elements of taxation. Although most of the changes won’t apply to pass-through businesses, the new law represents the most sweeping change in U.S. tax law since the changes that were implemented in 1986.

“That was big, but this one is more complicated. This will result in more change,” Larsen said.

David Peek, an attorney at the Rogers Towers law firm who specializes in federal income tax, estate planning, estates and trusts, said that the new law is the biggest change in decades.

“I’ve been practicing for 39 years and this is the most massive piece of legislation I’ve seen in that time,” he said.

“It’s going to keep a lot of people up late at night — like me and accountants,” Peek added.

"What I’ve learned in 39 years, I have to forget and relearn.”