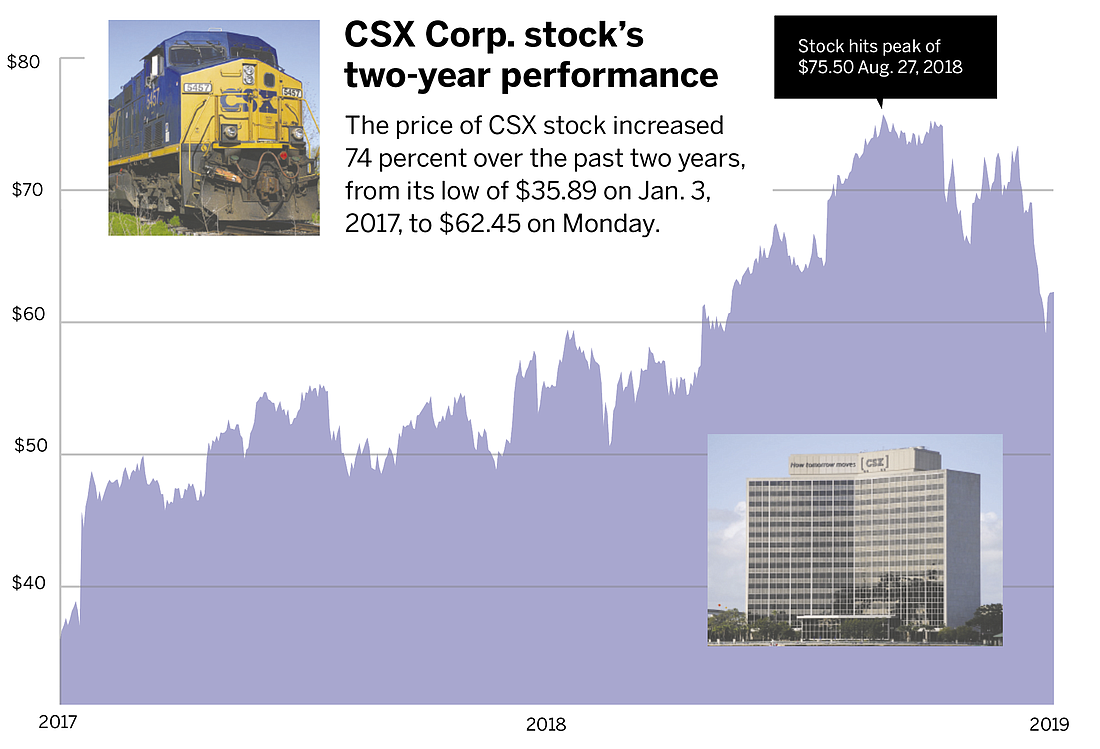

CSX Corp. has been the best performing Jacksonville-based company over the past two years, producing a shareholder return (stock price increase plus cash dividends) of 78 percent for 2017 through 2018.

However, one analyst downgraded the Jacksonville-based company last week because he sees better opportunities in other railroad stocks after the big run.

“CSX has materially outperformed the past two years as it generated by far the best EPS and free cash flow growth, and its margins improved from worst among the rails to first,” Wolfe Research analyst Scott Group said in a research note.

“We still expect good margin improvement and EPS growth to continue this year, but we see less potential EPS upside after 2018 benefited from a perfect storm of precision railroading, accessorial charges, real estate gains, export coal strength, and truckload capacity tightness,” he said.

Group downgraded CSX from “outperform” to “peer perform” even though “we still see good absolute upside for the stock from here.”

He said the downgrade has more to do with the potential for gains from two other major railroads, Norfolk Southern Corp. and Union Pacific Corp.

“Our long-standing investment thesis on the rails centers on buying the one with the most room for margin improvement,” he said.

Meanwhile, Morgan Stanley analyst Ravi Shanker on Monday raised his price target for CSX’s stock from $55 to $56, but that’s still below its recent trading level in the low $60s. He maintains an “underweight” rating on the stock.

“We believe the current backdrop for CSX’s turnaround is difficult as several key end markets face cyclical and secular threats (auto, coal, intermodal), pricing gains are decelerating, low hanging cost opportunities may have already been taken and shipper scrutiny and investor expectations are high,” Shanker said in a report on the overall transportation industry.

“We believe risk/reward is skewed to the downside from here,” he said.

Shanker’s also reiterated his “underweight” rating on Jacksonville-based trucking company Landstar System Inc.

“We believe the upside is more than priced in at Landstar given higher relative valuation vs. peers, which keeps us underweight,” he said.

Landstar’s stock price fell 8 percent last year but its overall return for 2017-18 was a positive 15 percent.

Web.com Group Inc. on Monday announced the hiring of Sharon Rowlands as chief executive officer, replacing the retiring David Brown.

Rowlands was CEO of ReachLocal Inc., a California-based digital marketing company that was sold to Gannett Co. Inc. in 2016. She later became president of USA Today Network Market Solutions while continuing to serve as CEO of ReachLocal.

ReachLocal was a public company that reported $160 million in revenue in the first half of 2016, before the buyout.

Rowlands, 60, is a native of the United Kingdom who has more than 20 years of experience leading technology companies, Web.com said.

Web.com founder David Brown announced his retirement as CEO last month, following the October sale of the company to affiliates of private equity firm Siris Capital Group LLC.

Rowlands will join Web.com on Jan. 28.

Tegna Inc. said Monday it has reached renewal agreements with the ABC network for all nine of its stations that are affiliated with the network, including WJXX TV-25 in Jacksonville.

The agreement is a “multi-year deal,” the company said, but it did not specify the length of the contract.

Tegna also owns Jacksonville NBC affiliate WTLV TV-12. According to Tegna’s annual report, the affiliation agreement for WTLV runs through 2021.

Tegna owns a total of 49 stations in 41 markets.

Deutsche Bank analyst Ashish Sabadra Monday lowered his price target on Black Knight Inc. from $59 to $57, but maintained a “buy” rating with the stock trading at $45.38 at the time of his report.

Sabadra said in his research report he likes the Jacksonville-based provider of mortgage processing services for “its solid revenue growth, high revenue visibility, and stability in a volatile market.”

Black Knight dominates its field, providing mortgage processing for 62 percent of all U.S. first mortgage loans, and Sabadra said that number should reach 70 percent as the company implements pending contracts with more lenders.

However, Sabadra sees opportunities for Black Knight to increase market share in other areas.

“The company has only a 17 percent market share in second lien mortgage servicing software solutions and we estimate less than a 10 percent market share in origination software, which provides significant cross-sell opportunities,” he said.

“More importantly, there is opportunity to sell incremental solutions to the existing customer base, which along with pricing should drive higher revenue per mortgage serviced.”

Black Knight’s stock dropped sharply in November after the company announced it was acquiring a stake of less than 20 percent in business data firm Dun & Bradstreet, as investors worried about increased debt to pay for the investment.

But Sabadra sees a positive from Black Knight CEO Anthony Jabbour’s appointment to the additional role of CEO of Dun & Bradstreet, as part of the investment.

“Anthony Jabbour leading both companies will provide Black Knight insights into D&B business, ability to leverage best practices across both organizations, and help monitor the progress on the turnaround,” he said.

Even with the November drop, Black Knight’s stock rose 2 percent in 2018 in a bad year for the market and had a two-year return of 19 percent.

Marker Therapeutics Inc. was the best performer of all Jacksonville-based companies in 2018, rising 41 percent last year.

And the developer of cancer therapy treatments got off to a good start in 2019, rising $1.88, or 39 percent, to $6.65 last week after announcing progress in clinical trials.

The company was formed last year by the merger of Jacksonville-based TapImmune Inc. with Marker Therapeutics, with the merged company taking the Marker name.

Marker intends to move its headquarters office to Houston but as of now, it still lists its headquarters in Jacksonville in Securities and Exchange Commission filings.

The company has no products on the market and no revenue, but last week’s update said Marker has five clinical trials underway producing promising results.

Glowpoint Inc., which has agreed to merge into Jacksonville-based SharedLabs Inc., said Monday it is not in compliance with NYSE American stock exchange listing requirements but has been granted additional time to regain compliance.

SharedLabs had been planning an initial public offering but instead agreed in November to become public by merging with Denver-based Glowpoint. SharedLabs will be the surviving company after the merger of the two technology firms and become publicly traded.

Glowpoint’s stock has traded mostly below 20 cents a share for the past six months and the company received a deficiency letter from NYSE American in July saying it was not in compliance because of the low stock price.

The company faced a Jan. 5 deadline to regain compliance but because of the merger agreement with SharedLabs, the deadline was extended until Glowpoint’s annual meeting in May, the company said Monday.

Glowpoint said it will enact a reverse stock split before the merger to increase its price per share, which will allow it to meet NYSE American requirements.

The merger is expected to be completed in the spring, Glowpoint said. However, the merger agreement includes a go-shop period that allows Glowpoint to seek higher offers from other parties until Feb. 3.